WASHINGTON, May 4, 2026 —

Key Takeaways

- ACA Marketplace premiums increased by an average of 26% in 2026 — driven by the expiration of enhanced premium tax credits that had capped monthly costs at no more than 8.5% of household income since 2021, and by base-rate increases averaging 23% across all plans nationally.

- The maximum out-of-pocket limit for in-network care rose to $10,600 for a single individual in 2026 — a $1,400 increase from 2025 — meaning every American with ACA-compliant coverage, including employer-sponsored plans, faces higher exposure in a serious medical event this year.

- ACA Marketplace enrollment fell in 2026, with KFF warning that the departure of younger, healthier enrollees will create a death spiral effect — pushing 2027 premiums even higher as the remaining risk pool skews older and sicker.

Why Your Premium Jumped — the Two Forces Hitting at Once

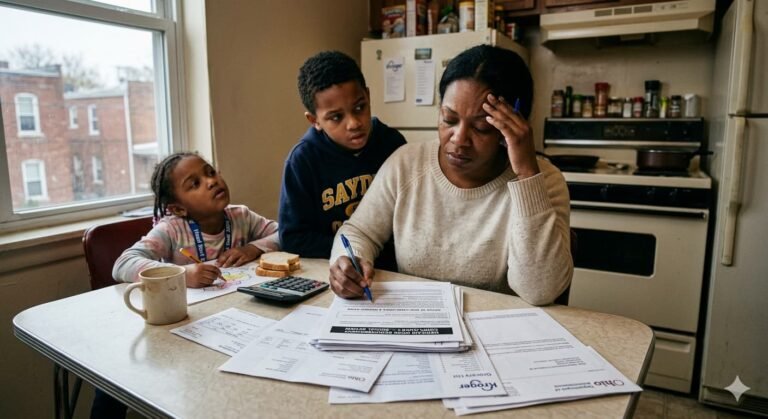

The 2026 premium surge is not one problem. It is two separate problems landing simultaneously, compounding each other in ways that are particularly painful for middle-income Americans.

The first is the expiration of enhanced premium tax credits. These credits were introduced during the COVID-19 pandemic in 2021 and extended through 2025. They capped what any ACA enrollee paid for a benchmark plan at no more than 8.5% of their household income — regardless of how high their income was. They also made people with incomes above 400% of the federal poverty level ($62,600 for an individual in 2026) eligible for subsidies for the first time. Congress did not renew them when they expired on December 31, 2025.

The second is that insurers raised their base premiums independently. Before subsidies, the average ACA plan increased 23% in 2026 — the largest base-rate increase since 2018. Insurers cited rising healthcare costs, high prescription drug prices, and the lingering utilization surge from the post-pandemic period as the primary drivers.

The combination of both forces hitting at once — subsidy expiration and base-rate increases — is what produced the 26% average increase in what enrollees actually pay. For someone who was paying $200 a month in 2025 under the enhanced subsidy structure, the same plan in 2026 may cost $400 or more.

Who Is Paying More — and by How Much

The impact is not uniform. It falls hardest on specific groups.

| Enrollee Group | 2025 Monthly Cost | 2026 Monthly Cost | Change |

|---|---|---|---|

| Income 100–150% FPL (individual ~$15–22K) | Near $0 with subsidies | Low — basic subsidies remain | Modest increase |

| Income 200–300% FPL (individual ~$30–45K) | Low with enhanced credits | Moderate — enhanced credits gone | Significant increase |

| Income 300–400% FPL (individual ~$45–62K) | Moderate with enhanced credits | High — full subsidy cliff | Sharp increase |

| Income above 400% FPL (individual $62K+) | Subsidized under enhanced rules | No subsidy — full premium | Largest increase |

| Adults 50–64 on ACA | Highest premiums but helped by credits | Full premium exposure | Most severe impact |

The 5 million Americans aged 50 to 64 who depend on ACA coverage face the sharpest absolute dollar increases. This group pays the highest base premiums — because ACA plans can charge older enrollees up to three times what younger enrollees pay — and was most dependent on the enhanced credits to make those premiums manageable. Without the credits, a 60-year-old earning $70,000 a year may face a benchmark plan costing $1,200 to $1,600 a month before subsidies in high-cost states.

The Navigator Shortage Making Everything Harder

Navigating the ACA Marketplace has always required some effort. In 2026 it requires significantly more — at precisely the moment when support infrastructure has been gutted.

Trained navigators — neutral, federally funded counselors who provide free help comparing plans, understanding subsidies, and enrolling in coverage — faced a 90% federal budget cut beginning in early 2025. Staffing reductions at the Centers for Medicare and Medicaid Services also reduced the number of government employees available to resolve coverage issues and answer enrollment questions. In the more than half of states where the federal government runs the marketplace, there are dramatically fewer people available to provide free, impartial enrollment help than in any prior year.

The practical consequence is that millions of Americans shopping for coverage in 2026 are doing so without the guidance that helped them navigate comparable decisions in prior years. They are more likely to make suboptimal plan choices — selecting lower premiums with higher deductibles that expose them to the full $10,600 out-of-pocket maximum, or gravitating toward non-ACA-compliant plans that do not cover pre-existing conditions and have no out-of-pocket cap.

The Junk Plan Trap — Why Low Premiums Can Be Dangerous

The combination of higher ACA premiums and reduced navigator support has created fertile ground for the marketing of non-ACA-compliant health plans. These plans — sold outside the official marketplace under names like association health plans, health sharing ministries, short-term plans, and farm bureau plans — offer dramatically lower monthly premiums that look appealing next to a marketplace plan that costs $400 or $600 a month.

What they do not offer: coverage for pre-existing conditions. Coverage of all essential health benefits. An annual out-of-pocket maximum. Guaranteed renewability. A network of providers that must meet federal adequacy standards.

A 55-year-old with a prior cancer diagnosis who enrolls in a health sharing ministry plan to save $300 a month may discover, after a recurrence, that the plan considers cancer treatment a pre-existing condition and covers nothing. Federal law does not require these plans to cover what ACA plans must cover. State law varies widely. The savings are real until a claim is filed. Then the exposure is potentially unlimited.

The 2027 Preview — Why This Gets Worse Before It Gets Better

The departure of younger, healthier enrollees from the ACA marketplace in 2026 — driven by premium shock — is not just a 2026 problem. It sets up a worse 2027.

Insurance pricing is fundamentally about risk pooling. When young, healthy people pay into a shared pool and use relatively little care, their premiums subsidize the higher costs of older, sicker enrollees. When premium increases drive healthy people out of the pool, the remaining enrollees generate higher average claims, which forces insurers to raise premiums again the following year to cover costs — which drives more healthy people out. This cycle is what insurance economists call a death spiral.

KFF warned explicitly in February 2026 that the coverage losses from enhanced subsidy expiration will push 2027 premiums even higher as the risk pool degrades. The November 2026 open enrollment period — which opens for 2027 coverage — will be the first full data point on how severe that degradation has become.

Pro Tips a Generic Article Would Miss

1. The benchmark plan used to calculate your subsidy may not be the cheapest plan available — and the difference can be substantial. ACA subsidies are calculated based on the second-lowest-cost Silver plan in your area. If you qualify for any subsidy, you can apply it to any metal tier. In 2026, many Bronze plans in high-premium markets cost less than the subsidy amount — meaning you can get a $0-premium plan with lower monthly costs if you are willing to accept higher deductibles. For healthy individuals who rarely use care, this can be an effective health insurance strategy that maximizes available retirement income planning flexibility.

2. The Special Enrollment Period triggered by losing coverage is 60 days — not 30. If you lost ACA coverage because you stopped paying premiums due to the premium shock or any other reason, you have 60 days from the loss of coverage date to enroll in a new plan. Most people believe the window is 30 days. The actual federal rule gives you 60. Knowing this distinction can be the difference between maintaining coverage and having a gap that exposes you to the full out-of-pocket maximum for any care received during the uninsured period.

3. If your employer offers health insurance that costs more than 9.02% of your household income in 2026, you may qualify for marketplace subsidies even if you have employer coverage available. The ACA’s affordability threshold — 9.02% of household income in 2026, down from 9.12% in 2025 — determines whether employer coverage counts as affordable. If your employer’s lowest-cost self-only plan exceeds that threshold, you qualify for marketplace subsidies instead. This rule catches many workers whose employer contributions are modest — particularly at small businesses and part-time positions — who assume incorrectly that having any employer coverage option makes them ineligible for marketplace assistance.

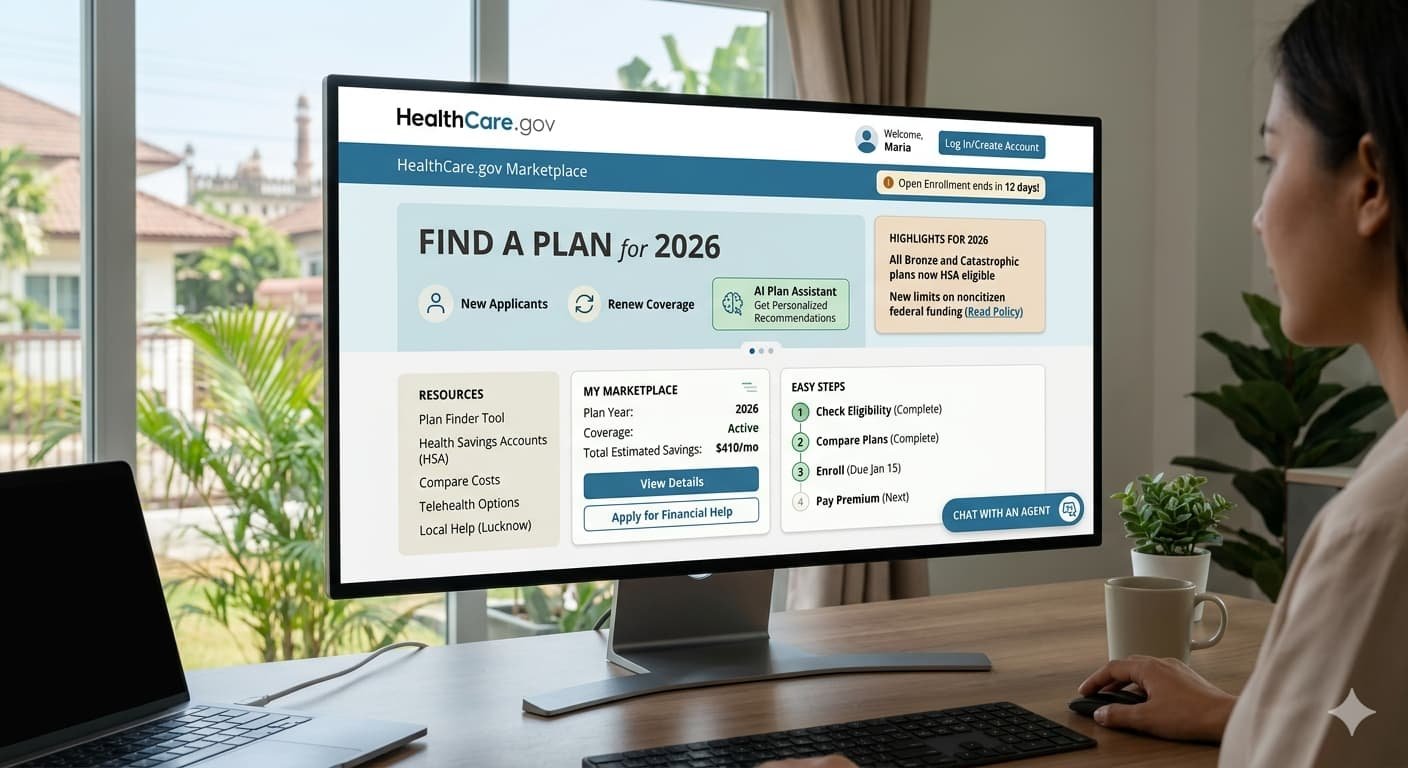

The most important action any American with ACA Marketplace coverage can take right now is to log into their state or federal marketplace account, verify their current plan’s premium and out-of-pocket structure for 2026, and compare it against other available options — particularly any Silver plans that may qualify for cost-sharing reductions based on their income. If your income is between 100% and 250% of the federal poverty level, cost-sharing reductions on Silver plans can dramatically reduce your deductible and out-of-pocket maximum even when headline premiums have risen. The comparison takes 20 minutes. The financial difference can run to thousands of dollars over the course of a year.

Frequently Asked Questions

Q: Why did ACA health insurance premiums go up so much in 2026? A: Two forces hit simultaneously. Enhanced premium tax credits that had capped costs since 2021 expired December 31, 2025, and insurers independently raised base premiums by an average of 23%. The combined effect produced a 26% average increase in what enrollees actually pay — the largest single-year increase since 2018.

Q: What is the ACA out-of-pocket maximum in 2026? A: The maximum out-of-pocket limit for in-network care increased to $10,600 for individuals and $21,200 for families in 2026, up from $9,200 and $18,400 in 2025. This applies to all ACA-compliant plans including employer-sponsored coverage.

Q: Do I still qualify for ACA subsidies in 2026? A: Basic premium tax credits remain available for individuals with incomes between 100% and 400% of the federal poverty level — approximately $15,000 to $62,600 for a single adult. The enhanced credits that extended eligibility above 400% FPL expired at year end. If your income is above $62,600, you likely pay full premium in 2026 without subsidy.

Q: Are non-ACA plans a good alternative to expensive marketplace plans? A: Generally no. Non-ACA-compliant plans — including short-term plans, health sharing ministries, and association health plans — offer lower premiums but do not cover pre-existing conditions, do not include all essential health benefits, and have no annual out-of-pocket cap. A serious illness can result in unlimited financial exposure under these plans.

Q: When is the next ACA open enrollment period? A: Open enrollment for 2027 coverage begins November 1, 2026 and ends December 15, 2026 — one month shorter than previous years. Coverage takes effect January 1, 2027 for enrollments completed by December 15.