WASHINGTON, May 10, 2026 —

Key Takeaways

- The Medicare Prescription Payment Plan, launched in January 2025 and continuing in 2026, allows all Medicare Part D enrollees to pay their out-of-pocket prescription drug costs in equal monthly installments throughout the year rather than in large, unpredictable amounts at the pharmacy counter — a structural change that directly addresses the cash flow crisis that drives many seniors to ration or skip medications in January and February.

- The plan interacts with the new $2,100 annual out-of-pocket cap that took effect January 1, 2026 — meaning a beneficiary who opts in can project their maximum annual drug exposure at $2,100, divide it by 12, and budget $175 per month as a firm ceiling on prescription costs regardless of what they actually take.

- The plan is not automatic for new enrollees — it requires an active opt-in with your Part D plan, either by phone or online — but once enrolled, it automatically renews each year unless you opt out, making the first enrollment decision the only significant action required.

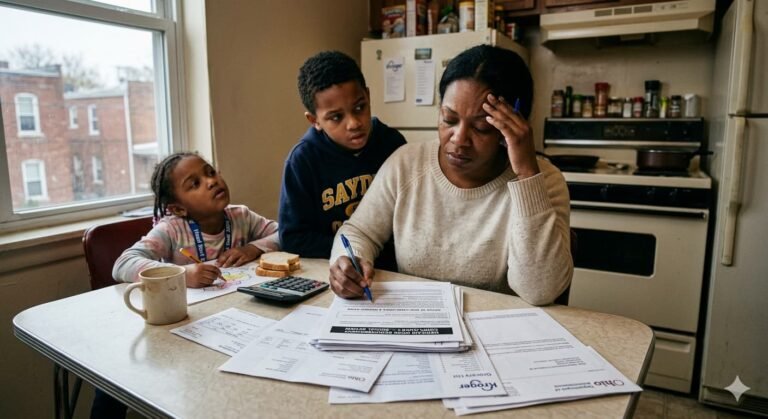

The January Drug Bill Problem the Payment Plan Solves

Every January, Medicare Part D beneficiaries who take expensive medications face a predictable financial shock that has no equivalent in any other insurance structure. The deductible — up to $615 in 2026 — must be paid before coverage begins. During the initial coverage phase, beneficiaries pay 25% coinsurance on covered drugs. For someone taking a specialty medication for cancer, rheumatoid arthritis, multiple sclerosis, or a similar condition, the bills that arrive in January and February can run to $1,000 or more per month before the annual out-of-pocket cap is reached and costs drop to zero.

The behavioral consequence is well-documented. Studies consistently show that patients facing large out-of-pocket drug costs at the start of the year skip doses, split pills, or delay refills at higher rates than patients facing the same annual costs spread in smaller monthly amounts. The medication adherence problem generated by front-loaded drug costs produces worse health outcomes — more emergency room visits, more hospitalizations, more complications — that cost Medicare more than the drug costs they were trying to avoid.

The Medicare Prescription Payment Plan was designed specifically to break this cycle. It does not reduce what you pay over the course of a year. It changes when you pay it. For beneficiaries whose cash flow cannot absorb a $1,500 January pharmacy bill but can absorb $125 per month, the timing difference is the difference between taking the medication and going without.

How the Plan Actually Works — Step by Step

The mechanism is straightforward. At the start of the year, your Part D plan estimates your total projected out-of-pocket drug costs for the full year based on your medication list and your plan’s cost-sharing structure. That projected total is divided by the number of months remaining in the year at the time you enroll and spread into equal monthly payments.

| Projected Annual Drug Cost | Monthly Payment (12 months) | Monthly Payment (starting July) |

|---|---|---|

| $1,200 | $100 | $200 |

| $1,800 | $150 | $300 |

| $2,100 (at cap) | $175 | $350 |

| $2,400 | $200 | $400 |

| $3,000 | $250 | $500 |

You continue picking up prescriptions at the pharmacy exactly as before — presenting your insurance card, receiving your medication. The plan pays the pharmacy immediately. You pay the plan your monthly installment separately, typically through automatic bank draft or a monthly bill. The pharmacy experience does not change. Your budget experience changes significantly.

The plan recalculates your installment amount at key points during the year — when you add or remove medications, when your coverage phase changes, or when you hit the $2,100 out-of-pocket cap and your costs drop to zero. If you reach the cap before year-end, your monthly installments stop immediately. You will not continue paying installments for costs you will no longer incur.

The $2,100 Cap — How It Interacts With Everything Else

The annual out-of-pocket cap of $2,100 in 2026 — increased from $2,000 in 2025 — is the most significant structural protection in Medicare’s prescription drug benefit. Understanding exactly what counts toward it and what does not is the difference between accurately projecting your drug costs and being surprised mid-year.

What counts toward the $2,100 cap:

- Your Part D deductible payments

- Your 25% coinsurance payments during the initial coverage phase

- Payments made on your behalf through Extra Help/Low Income Subsidy

- State Pharmaceutical Assistance Program contributions in some cases

What does NOT count toward the $2,100 cap:

- Your monthly Part D plan premium

- Costs for drugs not covered by your plan’s formulary

- Costs for drugs purchased outside your plan’s network pharmacy

- Over-the-counter medications not covered by Part D

The practical implication is that a beneficiary whose plan has a $615 deductible, who then pays 25% coinsurance on $6,140 worth of covered drugs — reaching the $2,100 cap ($615 deductible + $1,485 in 25% coinsurance on $5,940 in drug costs) — pays $0 for all remaining covered prescriptions through December 31. The higher the cost of your medications, the faster you reach the cap, and the more valuable the months of zero-cost coverage become.

The Negotiated Drug Prices That Lower the Cap Faster

Nine million Medicare beneficiaries take one or more of the 10 drugs whose prices were negotiated under the Inflation Reduction Act and which took effect January 1, 2026. For these beneficiaries, the interaction between negotiated prices and the $2,100 cap produces an outcome that was not mathematically possible in prior years.

Before negotiation, a beneficiary taking Eliquis — the most prescribed of the 10 drugs, used for blood clot prevention in atrial fibrillation — faced monthly out-of-pocket costs that varied widely by plan but could run to several hundred dollars per month. At those rates, reaching the $2,100 annual cap might take eight or nine months.

At the newly negotiated Maximum Fair Price, the same beneficiary’s monthly cost falls below $100. At that rate, reaching the $2,100 cap requires spending $2,100 on all covered drugs combined — which for a beneficiary taking only Eliquis and perhaps one other medication might take the full year or might not happen at all. The negotiated price effectively lowers the beneficiary’s annual drug bill below the cap threshold, meaning the cap’s zero-cost provision may not even be needed.

The payment plan, the cap, and the negotiated prices form a three-part system. Understanding how all three interact for your specific medication list is worth a 20-minute conversation with your Part D plan’s pharmacist or member services line — the calculation is specific to your drugs, your plan, and your coverage phase timing.

How to Enroll in the Payment Plan — and When Not To

Enrollment in the Medicare Prescription Payment Plan requires an active opt-in. You cannot be automatically enrolled without your consent. To enroll:

Call your Part D plan’s member services number — found on your insurance card or plan materials — and request enrollment in the Medicare Prescription Payment Plan. Most plans also allow online enrollment through their member portal. Enrollment can happen at any time during the year, and your installment amount will be calculated based on the remaining months.

The plan makes most financial sense for beneficiaries who expect to spend more than $1,200 in total annual out-of-pocket drug costs — those who will reach or approach the $2,100 cap. For beneficiaries whose annual drug costs are modest — under $600, say — the administrative overhead of managing a monthly payment relationship with the plan may not justify the benefit, since the front-loading problem is less severe when the annual cost is lower.

The plan also makes sense only if your cash flow actually benefits from spreading costs. A beneficiary with a substantial savings account who pays attention to their monthly statements and can absorb a $1,000 January pharmacy bill without financial stress may find the administrative simplicity of paying at the counter preferable to managing monthly installments. The plan is a tool for people whose financial situation makes front-loaded costs genuinely difficult — not a universally superior approach.

Pro Tips a Generic Article Would Miss

1. Enroll in the payment plan before your highest-cost month — not after. The payment plan calculates installments based on your remaining projected annual costs at the time of enrollment. If you enroll in January, the full annual projected cost is divided by 12. If you wait until May and have already paid $800 in out-of-pocket costs, only the remaining projected costs are spread over the remaining months — producing higher monthly installments. Earlier enrollment almost always produces lower monthly payments.

2. The payment plan’s automatic renewal means you need to actively opt out if your medication costs drop significantly in 2027. Once enrolled, the plan automatically re-enrolls you for the following year based on a notice sent before December 15. If your drug regimen changes in 2026 — a generic becomes available, a medication is discontinued, your condition changes — and your projected 2027 costs drop substantially, the automatic renewal may produce monthly installments that are higher than necessary. Review the renewal notice carefully each November and opt out if your circumstances have changed.

3. The Extra Help program — also called the Low-Income Subsidy — dramatically changes the cap calculation for qualifying beneficiaries, and most people who qualify are not enrolled. Extra Help provides Part D cost-sharing assistance for Medicare beneficiaries with limited income and resources. In 2026, qualifying beneficiaries pay no more than $4.50 for generic drugs and $11.20 for brand-name drugs — regardless of the plan’s standard cost-sharing structure. The $2,100 cap still applies, but qualifying beneficiaries reach it far more slowly because their per-prescription costs are so much lower. Roughly 3 million people who qualify for Extra Help are not currently enrolled — check eligibility through your state Medicaid office or the Social Security Administration if your annual income is below approximately $22,000 for a single person.

The most valuable action any Medicare Part D enrollee with high prescription costs can take today is a call to their plan’s member services line with two questions: Am I currently enrolled in the Medicare Prescription Payment Plan, and based on my current medication list, what is my projected annual out-of-pocket cost for 2026? Those two data points — enrollment status and projected annual exposure — determine whether the payment plan makes sense for your situation and whether the $2,100 cap will be reached before year-end. The calculation is specific to your plan and your drugs. The plan’s pharmacist team is required to walk you through it. Five minutes on the phone can produce a number that shapes your entire healthcare budget for the rest of 2026.

Frequently Asked Questions

Q: What is the Medicare Prescription Payment Plan? A: It is a program that allows all Medicare Part D enrollees to pay their annual out-of-pocket prescription drug costs in equal monthly installments rather than in large amounts at the pharmacy counter. It launched in January 2025 and continues in 2026. It requires an active opt-in but automatically renews each year unless you opt out.

Q: What is the Medicare Part D out-of-pocket cap for 2026? A: The annual out-of-pocket cap for covered Part D drugs is $2,100 in 2026, up from $2,000 in 2025. Once you reach this amount, covered prescriptions cost $0 for the rest of the calendar year.

Q: How do I enroll in the Medicare Prescription Payment Plan? A: Call your Part D plan’s member services number or log into your plan’s online member portal and request enrollment. You can enroll at any time during the year. Your plan will calculate equal monthly installments based on your remaining projected annual drug costs.

Q: Does the Medicare Prescription Payment Plan reduce what I pay? A: No. It changes when you pay, not how much you pay. Your total annual out-of-pocket drug costs remain the same — the plan spreads those costs into predictable monthly installments rather than front-loading them at the pharmacy counter.

Q: Who benefits most from the Medicare Prescription Payment Plan? A: Beneficiaries who take expensive medications and face large pharmacy bills in January and February — particularly those whose annual drug costs are projected to exceed $1,200 — benefit most. The plan is designed for people whose cash flow makes front-loaded costs genuinely difficult to manage.