WASHINGTON, June 11, 2026 —

Social Security retirement benefits feel like the bedrock of American retirement security. They are inflation-adjusted, guaranteed, and — most people assume — untouchable. Most people are wrong about that last part in one very specific situation.

Federal student loan debt in default can trigger a Treasury Offset that reduces every Social Security payment by up to 15% until the balance is repaid. The mechanism is called the Treasury Offset Program. It requires no court judgment, no lawsuit, and no warning beyond a single offset notice that arrives after the reduction has already been scheduled. For the 1.7 million Americans over age 50 who hold defaulted federal student loans — many of them borrowers who took loans for their own education decades ago, others who borrowed for children’s educations under the Parent PLUS program — the resumption of federal loan collections in 2026 makes this risk acutely current.

How Treasury Offset Works — the Mechanics Behind the Reduction

Federal student loan borrowers enter default when they fail to make a required payment for 270 days. Under normal circumstances, the loan servicer reports the default to the Department of Education, which refers the debt to the Treasury Department’s Bureau of the Fiscal Service. The Bureau’s Treasury Offset Program matches defaulted borrowers against federal payment databases — including Social Security benefit records — and automatically redirects a portion of those payments to the creditor agency before depositing the remainder in the borrower’s account.

The entire process happens without a court proceeding. There is no judge. There is no hearing unless the borrower requests one. The offset begins after a 60-day notice window during which the borrower can challenge the offset or take corrective action. If no action is taken, the offset begins with the next monthly payment.

The maximum garnishment for student loans is 15% of the monthly Social Security benefit, or the amount by which the benefit exceeds $750, whichever is less. On the average 2026 retirement benefit of $2,071 per month, 15% equals $310.65 — reducing the monthly check to $1,760.35. For a beneficiary receiving $900 per month, the garnishable amount is the lesser of $135 (15% of $900) or $150 (the amount by which $900 exceeds the $750 floor) — meaning $135 would be withheld monthly. For any beneficiary receiving exactly $750 or less, no garnishment is permitted.

Why This Risk Is Escalating in 2026

The federal student loan collection system was effectively frozen for more than five years. The pandemic-era forbearance that began in March 2020 paused collections, interest accrual, and Treasury Offset Program referrals for all federal student loans. That pause was gradually unwound between 2023 and 2025 — and then complicated further by the SAVE plan litigation, which placed millions of borrowers in administrative forbearance again while the courts resolved the plan’s legality.

With the SAVE plan permanently terminated by court order on March 10, 2026, and the administrative forbearance that accompanied the SAVE litigation ending on August 1, 2026 for affected borrowers, the full federal collection apparatus is returning to operation. Loan servicers are resuming default reporting. The Department of Education is resuming Treasury Offset Program referrals for borrowers whose loans have been in default since before the pandemic pause. And the notice clock — the 60-day window before offset begins — is now running for a cohort of borrowers who have not received a collection communication in years.

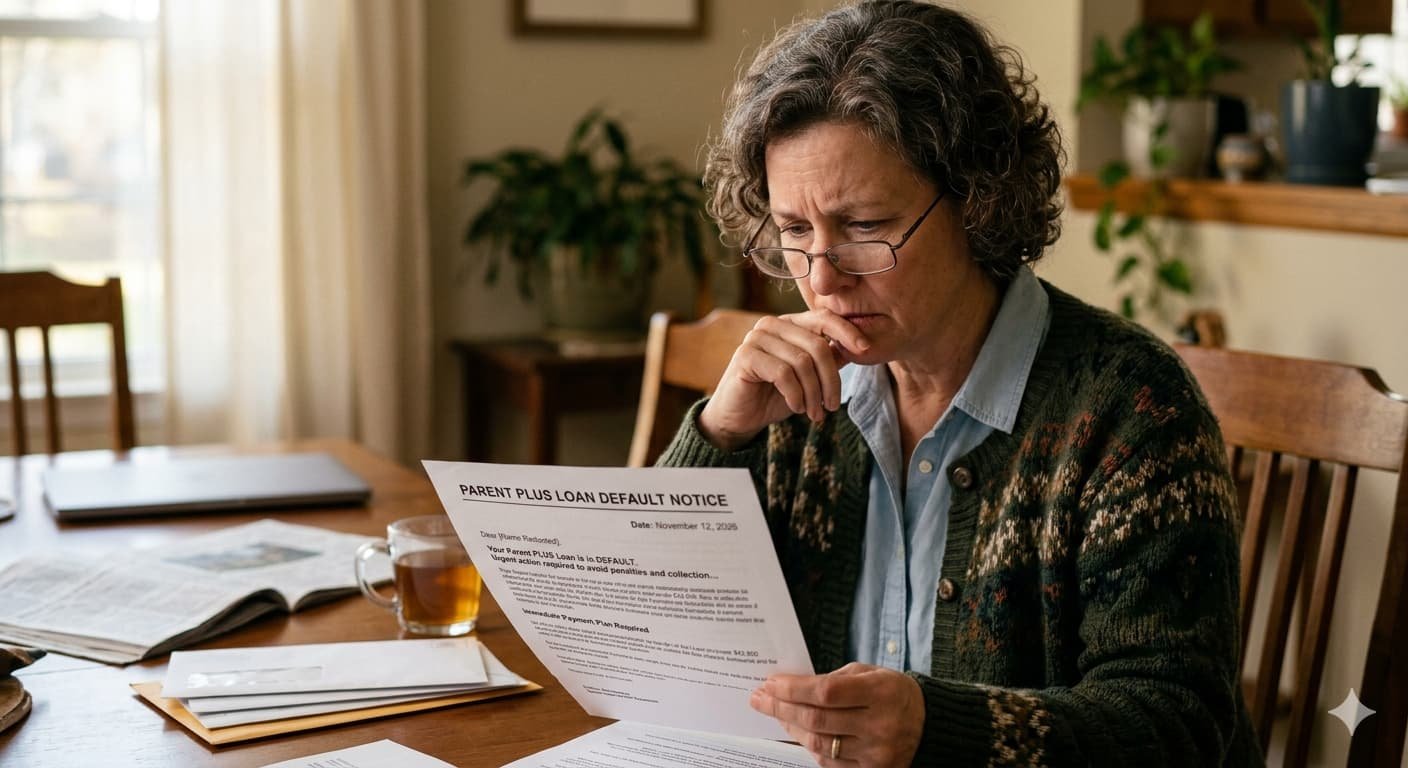

The borrowers most at risk are those who entered default before the pandemic pause and who are now collecting or approaching Social Security age. Parent PLUS loan borrowers — parents who took federal loans to fund their children’s educations and who are now in their 60s and 70s — represent a particularly exposed population. Parent PLUS loans have no income-driven repayment options at initial origination, carry higher interest rates than direct student loans, and are issued to borrowers who may have limited retirement income beyond Social Security.

The Three Specific Actions That Stop Garnishment Cold

The Treasury Offset Program can be stopped at any stage before it begins — and can be reversed quickly even after it has started — through three specific mechanisms that most affected borrowers have never been told about.

Rehabilitation is the fastest path to stopping an offset and removing the default status from the borrower’s credit report. A defaulted direct loan or FFEL loan can be rehabilitated by making nine voluntary, consecutive, on-time monthly payments within a 10-month window. The payment amount is set at 15% of discretionary income — the same formula as income-driven repayment — and cannot exceed the standard 10-year repayment amount. For a borrower with low retirement income, the calculated rehabilitation payment can be as low as $5 per month. After nine consecutive payments, the default status is removed, the loan is transferred to a new servicer, and Treasury Offset Program referrals stop.

Loan consolidation is an alternative that does not require nine payments but produces a less favorable credit outcome. Consolidating a defaulted loan into a new Direct Consolidation Loan eliminates the default status immediately and makes the new loan eligible for income-driven repayment plans. The Trade-off: consolidation does not remove the original default from the credit report — it simply closes the defaulted account and opens a new one. For borrowers whose primary concern is stopping the Social Security offset rather than credit repair, consolidation can accomplish that goal more quickly than rehabilitation.

A hardship hearing request, filed within 60 days of the offset notice, temporarily suspends the offset while the request is reviewed. The hearing is not a court proceeding — it is an administrative review that allows the borrower to present financial hardship documentation or to dispute the validity of the debt. If the borrower can demonstrate that the offset would render them unable to meet basic living expenses, the offset may be reduced or suspended pending repayment negotiations. This is the least reliable of the three options — hearing outcomes vary — but it preserves the 60-day window during which other remedies can be pursued.

| Social Security Garnishment for Student Loans — Key Facts | Detail |

|---|---|

| Maximum garnishment | 15% of monthly Social Security benefit |

| Protected floor | Benefits below $750/month cannot be garnished |

| Garnishment on $2,071/month average | Up to $310.65/month |

| Garnishment on $900/month benefit | Up to $135/month |

| Legal requirement | No court order needed — administrative offset |

| Notice period before offset begins | 60 days from offset notice |

| Trigger | Federal student loan in default (270+ days past due) |

| Collection pause | March 2020 – phased resumption through 2025-26 |

| Borrowers over 50 with defaulted loans | ~1.7 million |

| Stop garnishment option 1 | Rehabilitation — 9 payments (as low as $5/month) |

| Stop garnishment option 2 | Direct Consolidation Loan — eliminates default |

| Stop garnishment option 3 | Hardship hearing — suspends offset 60 days |

| SAVE plan status | Terminated March 10, 2026 |

| Interest restart for SAVE borrowers | August 1, 2026 |

| Parent PLUS borrower exposure | High — limited IDR options, higher rates |

Pro Tips a Generic Article Would Miss

1. The 60-day notice window is the most valuable time in a default — and most borrowers treat it as a countdown rather than a window of action. When the Department of Education sends the 30-day offset notification — the letter that tells a borrower a Treasury offset is scheduled — a 60-day response window opens. Within that window, a borrower who contacts their servicer and enters a rehabilitation agreement stops the offset before it ever begins. The first rehabilitation payment in that 60-day period does not need to be large. It needs to exist and be processed by the servicer before the offset activation date. Borrowers who receive an offset notice should call their servicer on the day the letter arrives, request the rehabilitation intake process, and confirm in writing that the intake has been received. That conversation, made within 60 days, is the difference between an offset that never happens and one that takes months of paperwork to reverse.

2. Parent PLUS loans are the most commonly misunderstood category of borrower in the Social Security garnishment risk profile — and the parents who took them often do not know that their own retirement benefit is collateral. Parent PLUS borrowers took loans in their own name, using their own credit, for their children’s education. The child’s degree does not shield the parent’s Social Security check. If the parent borrower defaults on a Parent PLUS loan, their Social Security benefit faces the same 15% offset as any other federal student loan default — regardless of whether the child is employed and earning income. Parents who took Parent PLUS loans and are approaching retirement should check their current loan status through studentaid.gov before their first Social Security benefit is deposited.

3. The Social Security Administration sends a notice before the offset begins — and that notice is the most important piece of mail a borrower can receive, but it goes to the address on file with SSA, not necessarily the address the borrower currently uses. The offset notice goes to the address the Social Security Administration has on record. For retirees who have moved, the letter may go to an old address. The borrower receives no offset and has no opportunity to act in the 60-day window — because they never received the notice. Checking and updating the address on file with SSA through ssa.gov, and separately confirming current contact information with the student loan servicer through studentaid.gov, is the single most important preventive action any borrower approaching retirement age can take before the collection system catches up with their account.

FAQ

Q: Can the government really take my Social Security for student loans? A: Yes. Federal student loans in default can trigger a Treasury Offset Program collection that reduces your Social Security benefit by up to 15% per month. No court order is required. The offset begins after a 60-day notice period. Private student loans cannot be collected through Social Security offsets — only federal loans. The $750 monthly floor protects the lowest-income beneficiaries from complete garnishment.

Q: How do I find out if my federal student loans are in default? A: Log in to studentaid.gov using your FSA ID. Your loan status is displayed in your account dashboard. A loan in default will be listed as such. You can also call the Default Resolution Group at the Department of Education directly. If your loan was transferred to a private collection agency, that agency’s contact information will also be in your studentaid.gov account.

Q: What is the fastest way to stop a Social Security offset for student loans? A: Enter a rehabilitation agreement immediately. Contact your loan servicer, request the rehabilitation intake process, and make your first payment within the 60-day notice window. Nine consecutive monthly payments — as low as $5 per month for low-income borrowers — remove the default status and stop the offset. If consolidation is faster in your specific servicer’s timeline, a Direct Consolidation Loan also stops the offset, though it does not remove the default from your credit history.

Q: What is the protected amount that cannot be garnished? A: Social Security benefits below $750 per month cannot be garnished for student loans under any circumstances. Above $750, the garnishable amount is the lesser of 15% of the total benefit or the amount by which the benefit exceeds $750. A beneficiary receiving $820 per month can have no more than $70 per month offset — the amount above $750 — even though 15% of $820 would be $123.

Q: Are Supplemental Security Income payments protected from student loan offsets? A: Yes. SSI payments — the needs-based disability and retirement program for low-income individuals — are fully protected from Treasury Offset Program collections and cannot be reduced for any federal debt, including student loans. The garnishment risk applies specifically to Social Security retirement, survivor, and disability insurance benefits, not to SSI.

If you are over 55, hold federal student loans, and are uncertain whether those loans are in default or approaching default, checking your status today at studentaid.gov is the most important action in this article. The federal collection system has been on pause for years. It is coming back online. The 60-day window that protects your Social Security check is only available if you know it exists before the notice arrives.