WASHINGTON, April 27, 2026 —

Key Takeaways

- Nebraska becomes the first state in the country to enforce Medicaid work requirements starting May 1, 2026 — eight months before the federal January 2027 deadline — requiring low-income adults in the ACA Medicaid expansion group to document 80 hours per month of work, job training, education, or community service to maintain coverage.

- The Congressional Budget Office projects the work requirements alone will result in 7.5 million Americans losing health insurance by 2034 — with the broader package of Medicaid changes in the One Big Beautiful Bill Act projected to leave 10 million people uninsured through approximately 15 separate provisions that restrict eligibility, reduce federal funding, or both.

- The 40 states that expanded Medicaid under the Affordable Care Act now face a permanently reduced federal matching rate — forcing them to shoulder a greater share of costs for adults earning under $21,000 a year, creating fiscal pressure that could trigger additional state-level eligibility cuts independent of the federal work requirement.

What Medicaid Work Requirements Actually Require

The One Big Beautiful Bill Act, signed into law on July 4, 2025, introduced work requirements for adults in the ACA Medicaid expansion group — specifically, adults without dependent children and parents or caretaker relatives who gained coverage through the expansion of Medicaid eligibility to 138 percent of the federal poverty level. These are working-age adults who are not elderly or disabled but whose incomes qualify them for Medicaid in the 40 states that expanded the program.

Starting January 1, 2027, those adults will be required to document at least 80 hours per month of qualifying activity — employment, job search, job training, education, or community service — to maintain eligibility. Failure to document those hours results in loss of coverage. The requirement does not exempt people who are employed in seasonal or irregular work, whose jobs offer fewer than 80 hours per month, or who have documentation challenges common among low-income populations — such as limited digital access, language barriers, or unstable housing.

Nebraska has chosen not to wait until the federal deadline. The state announced it will begin enforcing work requirements on May 1, 2026 — the first in the country to do so, ahead of formal guidance from the Centers for Medicare and Medicaid Services on exactly how the requirements should be implemented. That means Nebraska is writing its own implementation playbook before the federal rulebook exists, a risk that state officials have acknowledged and accepted.

Who Gets Cut — and the Math Behind the 10 Million

| Medicaid Change | Policy | Projected Coverage Loss |

|---|---|---|

| Work requirements (ACA expansion adults) | 80 hrs/month documentation required | 5.3 million by 2034 |

| More frequent eligibility redeterminations | ACA expansion adults checked more often | Incremental losses |

| Restricted immigrant eligibility | Limits on lawfully present non-citizens | Significant but not fully quantified |

| Reduced federal match rate (FMAP) | States cover more costs for expansion adults | State-level cuts likely to follow |

| Provider tax restrictions | Limits states’ financing flexibility | Reduces state ability to fund Medicaid |

| Paused Biden-era enrollment rules | Streamlined enrollment processes halted | Procedural barriers increase |

| Total projected uninsured from all OBBBA changes | Combined effect of ~15 provisions | ~10 million by 2034 |

The single largest driver of coverage loss is the work requirement — responsible for an estimated 5.3 million of the 10 million projected to lose insurance. The second largest is administrative churn: requiring more frequent eligibility redeterminations means more people falling off coverage not because they are ineligible, but because they fail to complete paperwork on time. Research on previous Medicaid redetermination cycles — including the post-pandemic unwinding that ended in 2024 — consistently shows that a significant share of people who lose coverage during redetermination periods are actually still eligible; they simply missed a form or a deadline.

A University of Pittsburgh professor and health policy expert told Newsweek that the changes to Medicaid overall will result in approximately 10 million low-income people losing insurance coverage through the roughly 15 separate provisions that limit coverage, reduce federal spending, or both.

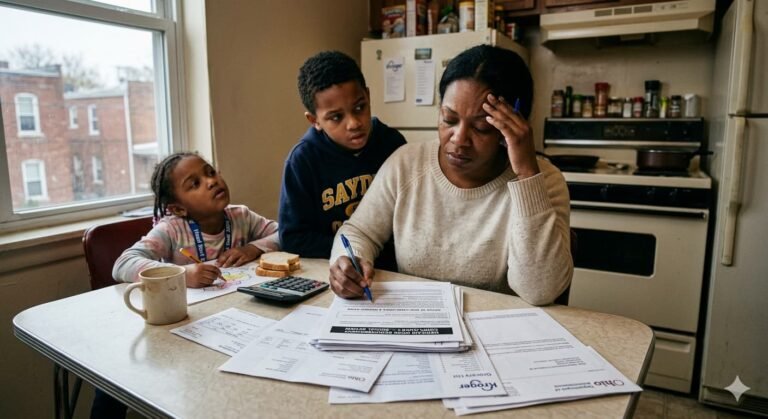

What Happens to People Who Lose Medicaid

The assumption embedded in work requirement legislation is that people who lose Medicaid will either find employer-sponsored insurance or purchase coverage on the ACA marketplace. The evidence from prior work requirement experiments does not support that assumption.

Arkansas implemented Medicaid work requirements in 2018 — the first and most extensively studied example in U.S. history. Within six months, more than 18,000 people lost coverage. A Harvard-led study found that the overwhelming majority of those who lost coverage did not gain other insurance. They became uninsured. Most were already working, but in jobs that did not offer employer coverage and that generated earnings too irregular to consistently document 80 hours per month. The Arkansas program was struck down by federal courts before it could be fully implemented.

The OBBBA work requirements are structured differently and are unlikely to face the same legal challenge — but the population losing coverage is demographically similar. Adults in the ACA expansion group who earn under 138 percent of the federal poverty level are disproportionately employed in part-time, seasonal, gig, or cash-based work. The documentation burden falls hardest on the people for whom documentation is most difficult.

The ACA Marketplace Gap — and Why It’s Getting Bigger

When people lose Medicaid, the theoretical safety net is the ACA marketplace. The problem in 2026 is that the enhanced premium tax credits that made marketplace coverage affordable — introduced during the pandemic and extended through 2025 — were not renewed by Congress. Their expiration means marketplace premiums have risen sharply for the income group that sits just above Medicaid eligibility.

A single adult earning $22,000 a year — just above the Medicaid cutoff in an expansion state — now faces a benchmark marketplace premium that, without enhanced subsidies, can consume 15 to 20 percent of their gross income. At that cost, many will simply go without coverage. The coverage gap — which affects people who earn too much for Medicaid but too little to afford marketplace plans without subsidies — has widened materially in 2026.

The CBO’s projection that 1.3 million more Americans will be uninsured in 2026 specifically reflects this dynamic, separate from the 10 million longer-term projection driven by the OBBBA’s structural changes to Medicaid.

The Rural Hospital Crisis Embedded in the Numbers

One consequence of Medicaid cuts that rarely makes headlines but carries serious long-term implications is the effect on rural hospitals. Rural hospitals operate on thin margins — often serving populations that are disproportionately covered by Medicaid. The reimbursements those hospitals receive for treating Medicaid patients help them stay open, pay staff, purchase diagnostic equipment, and maintain emergency services.

When Medicaid enrollment falls and reimbursement rates decline, rural hospitals absorb both a volume shock — fewer paying patients — and a revenue shock from reduced federal and state funding. The OBBBA’s restrictions on provider taxes — a financing mechanism states use to draw down additional federal Medicaid dollars — compounds this pressure by reducing the total pool of money available to hospitals serving low-income patients.

Several hospital associations have projected that the combination of reduced Medicaid reimbursement, lower enrollment, and provider tax restrictions will push a significant number of rural hospitals toward closure or service consolidation by 2028. Communities that lose their only hospital typically do not regain one. The coverage statistics tell part of the story. The infrastructure that delivers the care those statistics represent tells the rest.

Pro Tips a Generic Article Would Miss

1. If you’re in a Medicaid expansion state and work irregular hours, start documenting now — before your state’s deadline. Nebraska’s May 1 enforcement date is a preview of what every expansion state will face by January 2027. Keep a log of work hours, job search activities, training courses, and volunteer hours with dates. Screenshots, pay stubs, employer contact information — anything timestamped. The burden of proof is on the enrollee, not the agency. Starting documentation now gives you a clean record before enforcement begins.

2. The ACA marketplace has a Special Enrollment Period for people who lose Medicaid. If you lose Medicaid coverage due to work requirement enforcement or a redetermination, you qualify for a 60-day Special Enrollment Period to purchase marketplace coverage. This window opens at the date of coverage loss, not the date you receive the termination notice. Missing it means waiting until the next open enrollment period, which for 2027 coverage begins October 15, 2026.

3. GLP-1 drugs like Ozempic and Wegovy are now covered by both Medicare and Medicaid — but enrollment changes could affect access. The BALANCE Model announced by the Trump administration aims to expand GLP-1 coverage in Medicaid by negotiating lower prices with manufacturers. For the 10 million people projected to lose Medicaid coverage, access to these drugs — which can cost $1,000 to $1,350 per month without insurance — will effectively disappear unless they find other coverage. If you are currently receiving GLP-1 medications through Medicaid, your access to this treatment is directly tied to maintaining your eligibility.

If you or someone in your household is covered by Medicaid in an ACA expansion state, the single most important action you can take right now is to verify your current enrollment status directly with your state Medicaid agency — not your insurer, not a third party. Confirm that your contact information on file is current, that you have received and responded to any redetermination notices, and that you understand what documentation your state will require for work requirement compliance. The federal deadline is January 2027. Nebraska’s deadline is May 1. Other states will move at their own pace. The time to verify is before the notice arrives — not after.

Frequently Asked Questions

Q: What are the Medicaid work requirements in 2026? A: The One Big Beautiful Bill Act requires adults in the ACA Medicaid expansion group — without dependent children — to document at least 80 hours per month of work, job training, education, or community service to maintain coverage. The federal deadline is January 1, 2027. Nebraska begins enforcing the requirement May 1, 2026.

Q: How many people will lose Medicaid coverage from the new rules? A: The Congressional Budget Office projects the work requirements alone will result in 7.5 million Americans losing coverage by 2034. The full package of Medicaid changes in the OBBBA — across approximately 15 provisions — is projected to leave 10 million people uninsured.

Q: What happens if I lose Medicaid — can I get marketplace coverage? A: Yes. Losing Medicaid coverage triggers a 60-day Special Enrollment Period for ACA marketplace plans. However, enhanced premium tax credits that made marketplace plans affordable expired at the end of 2025 and were not renewed, making premiums significantly higher for low-income adults in 2026.

Q: Which states are implementing Medicaid work requirements first? A: Nebraska announced it will begin enforcement on May 1, 2026 — the first state in the country to do so. Other states can implement before the federal January 2027 deadline if they choose. States that have expressed interest in early implementation include Georgia, which already had a partial work requirement waiver, and several other Republican-led states.

Q: Do Medicaid work requirements apply to elderly or disabled enrollees? A: No. Work requirements under the OBBBA apply specifically to adults in the ACA Medicaid expansion group who are not elderly, not disabled, and do not have dependent children. Traditional Medicaid for elderly and disabled enrollees operates under different rules and is not subject to these work requirements.