WASHINGTON, MARCH 19, 2026 —

Key Takeaways

- ACA marketplace premiums are rising an average of 26% in 2026 — the largest single-year increase in the program’s history — after enhanced federal subsidies expired

- Medicare drug prices are falling for the first time ever on 10 high-cost medications, with out-of-pocket costs dropping more than 50% for nearly 9 million seniors

- Employer-sponsored insurance costs are rising 9% in 2026 — the highest jump in 15 years — adding an estimated $617 to the average family’s annual premium bill

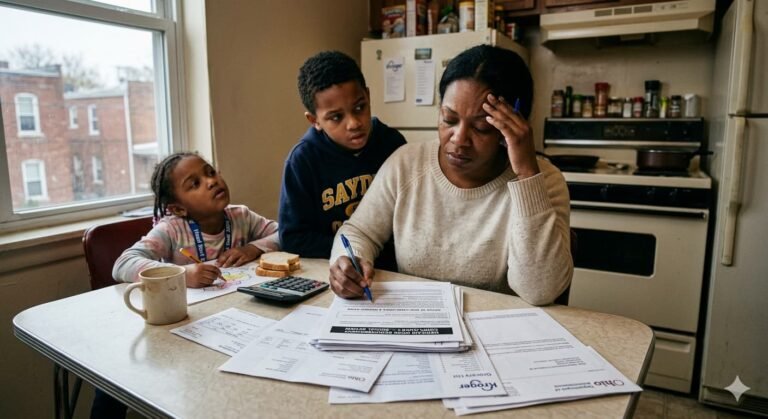

Nearly 250 million Americans will pay more for health coverage in 2026. That is not a projection — it is a confirmed reality that cuts across every type of insurance in the country. Medicare. Medicaid. ACA marketplace plans. Employer plans. Every category is more expensive this year than last.

But buried inside that broad picture is a divide that most Americans do not know about. If you are on Medicare, 2026 actually brings some of the most significant cost relief in the program’s history. If you are on the ACA or Medicaid, the picture is considerably darker. Understanding which side of that divide you are on — and what you can do about it — could save you thousands of dollars this year.

The ACA Collapse — 26% Premiums and No Subsidies

The biggest health insurance story of 2026 is the effective gutting of the Affordable Care Act marketplace. For four consecutive years, enhanced federal premium tax credits kept ACA plan costs artificially low — driving record enrollment and pushing millions of Americans’ monthly premiums to as little as $10. Those credits expired at the end of 2025, and Congress did not renew them.

The result is staggering. Average total premiums for Americans purchasing their own insurance through the ACA marketplace are rising 26% in 2026 — the highest out-of-pocket cost increase for any type of coverage in the program’s history. For a family that was paying $400 per month last year, that means a new bill closer to $504 per month — an extra $1,248 per year with no improvement in coverage.

Enrollment has already fallen in response. ACA marketplace enrollment dropped from more than 24 million in 2025 to fewer than 23 million in 2026 — the first decline in five years. Health policy experts expect the number of uninsured Americans to rise significantly through the rest of the year as more people decide the cost is simply not worth it.

The Medicare Drug Price Breakthrough

While ACA enrollees are absorbing the largest premium shock in the program’s history, Medicare beneficiaries are experiencing something that would have seemed impossible five years ago — falling drug prices.

The Inflation Reduction Act, signed by President Biden in 2022, gave Medicare the authority to negotiate prices directly with pharmaceutical companies for the first time in the program’s 60-year history. Those negotiated prices take effect January 1, 2026, covering the 10 most costly drugs in the Medicare program.

2026 Medicare Negotiated Drug Prices — What Changed

| Drug | Used For | Price Change |

|---|---|---|

| Eliquis | Blood thinner | Over 50% reduction |

| Xarelto | Blood thinner | Over 50% reduction |

| Jardiance | Diabetes | Over 50% reduction |

| Januvia | Diabetes | Over 50% reduction |

| Farxiga | Diabetes/Heart | Over 50% reduction |

| Entresto | Heart failure | Over 50% reduction |

| Enbrel | Arthritis | Over 50% reduction |

| NovoLog/Fiasp | Insulin | Over 50% reduction |

Nearly 9 million Medicare beneficiaries use at least one of these drugs. Seven of the eight will now cost less than $100 per month out of pocket. The Centers for Medicare and Medicaid Services projects total savings of $1.5 billion for enrollees in 2026 alone.

Employer Plans — The Hidden 9% Hit

Most working Americans get their health insurance through their employer and many assume their costs are insulated from the broader market turmoil. They are not. Employer-sponsored insurance premiums are rising 9% in 2026 — the largest increase in 15 years.

For a family plan, the average employee’s share of premiums was $6,850 in 2025. At 9% growth that rises to approximately $7,467 in 2026 — an additional $617 out of pocket every year, simply to maintain the same coverage. Deductibles, copays, and out-of-pocket maximums at most employer plans are also rising in parallel.

Health economists attribute the spike to a combination of factors — rising hospital costs, higher pharmaceutical spending, and the knock-on effect of Trump administration tariffs on medical devices and supplies. The uncertainty created by rapid policy changes in Washington has also driven insurers to price defensively, building larger margins into their 2026 premium calculations.

Medicaid — The 2027 Warning Every Low-Income American Needs to Hear Now

Medicaid cuts are already affecting states and enrollees in 2026, but the largest changes are still coming. The “One Big Beautiful Bill” signed by President Trump introduced a national work requirement for Medicaid expansion adults between the ages of 19 and 64 — requiring at least 80 hours per month of work, community service, or job training to maintain coverage. States must implement this requirement by December 31, 2026, with the full impact hitting in 2027.

The Congressional Budget Office projects the work requirement will remove approximately 5 million people from Medicaid coverage over 10 years. States that expanded Medicaid will no longer receive the temporary enhanced federal matching rate that made expansion financially attractive, adding budget pressure on governors across the country.

If you or someone in your household receives Medicaid, now is the time to understand what documentation your state will require for the work reporting requirement — before enrollment is at risk.

Pro Tips a Generic Article Would Miss

1. If you are on Medicare and take any of the 8 negotiated drugs — verify your pharmacy is applying the new price. Not all pharmacies updated their systems on January 1. Call your plan’s member services line and confirm your copay reflects the negotiated rate.

2. If you lost ACA coverage due to the premium increase — check your state’s Medicaid eligibility before going uninsured. In states that expanded Medicaid, the income threshold is 138% of the federal poverty level — approximately $20,783 for a single adult in 2026. Many people who are priced out of ACA plans qualify for Medicaid without knowing it.

3. If your employer raised your premium — ask HR about HSA eligibility. Starting in 2026, bronze and catastrophic marketplace plans now qualify as HSA-eligible high-deductible plans. Contributions to an HSA are tax-deductible, reducing your effective health care costs.

Actionable Steps

If you are on Medicare — log into medicare.gov and verify your current drug costs reflect the 2026 negotiated prices. If you are on an ACA plan — calculate your new monthly premium and compare it against your state’s Medicaid income threshold. If you have employer insurance — ask your HR department for your 2026 Summary of Benefits and Coverage document and check whether your plan qualifies for HSA contributions. Do not wait. Premium structures set in January will not change until open enrollment in October.