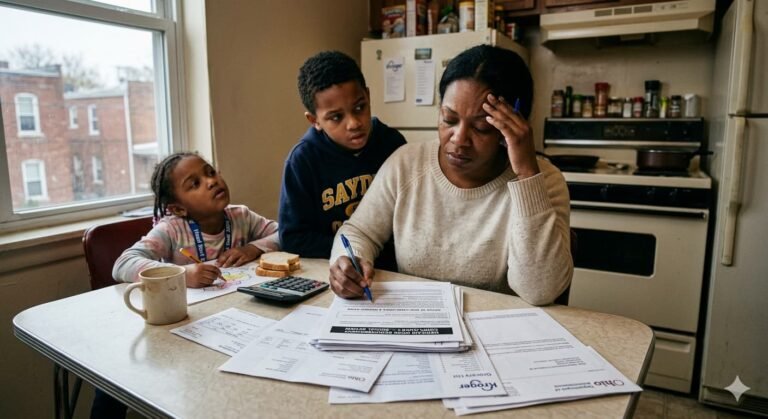

WASHINGTON, MARCH 17, 2026 — Standing at a pharmacy counter and watching the total climb past $300, $500, or even $1,000 for a single prescription is an experience tens of millions of Americans know too well. Two-thirds of Americans say they are very worried about their ability to pay for medications in 2026. Nearly one in four report difficulty affording their prescriptions. About 30% say they have skipped doses or rationed pills because of cost. The question that follows every one of those moments is the same: why does this keep happening?

The answer is not simple. But it is knowable — and understanding it is the first step toward doing something about it.

The Core Problem: No Price Controls

In most wealthy countries, governments negotiate directly with pharmaceutical companies to set drug prices. In Germany, France, the United Kingdom, Canada, and Japan, a centralized body evaluates each new drug’s clinical benefit and negotiates a price that reflects that value. The result is that Americans routinely pay two to three times more for the exact same drug, made by the exact same company, than patients in peer nations pay.

The United States does not do this — at least not for most of its population. Drug prices are set by manufacturers and negotiated privately between those manufacturers and insurance companies, pharmacy benefit managers, and hospital systems. No federal agency has the authority to simply cap what a drug company can charge. The market sets the price — and when patients need a medication to survive, market forces work very differently than they do for consumer goods.

Patents, Monopolies and the 20-Year Clock

At the heart of American drug pricing sits the patent system. When a pharmaceutical company develops a new drug, it receives a 20-year patent — an exclusive right to manufacture and sell the medication without competition. During that window, the company is the only seller. There is no competitor to undercut its price. Patients who need the drug have no alternative. That is a monopoly, and monopolies produce monopoly prices.

The patent clock starts running the moment a compound is identified — often years before it reaches patients. By the time a drug completes clinical trials, receives FDA approval, and reaches pharmacy shelves, a significant portion of its patent life has already elapsed. Companies price their drugs during the remaining patent window to recover not just the cost of developing that specific drug but also the cost of all the other compounds that failed in development — a number that, for major pharmaceutical companies, runs into the hundreds of failed experiments for every drug that succeeds.

When the patent expires, generic manufacturers can produce and sell identical versions of the drug at dramatically lower prices — often 80 to 85% less than the brand-name version. The problem is getting there. Brand-name manufacturers have become increasingly skilled at extending their exclusivity through what critics call patent thickets — filing dozens of additional patents on minor reformulations, delivery mechanisms, or dosage forms to push the generic entry date years further into the future.

The Hidden Players: PBMs and the Rebate System

Most Americans have never heard of a pharmacy benefit manager. That’s a problem, because PBMs — companies like Express Scripts, CVS Caremark, and OptumRx — sit at the center of every transaction between a drug manufacturer and an insured patient, and their financial incentives do not always align with lower prices.

PBMs negotiate rebates from drug manufacturers in exchange for placing their drugs on insurance formularies — the approved lists that determine which medications a plan will cover. Those rebates are calculated as a percentage of the drug’s list price. The higher the list price, the larger the rebate — and since PBMs keep a portion of those rebates, they have a financial incentive to favor high-list-price drugs over cheaper alternatives. The result is a system where a drug with a $500 list price and a $200 rebate can end up on an insurance formulary ahead of a competing drug that costs $150 with no rebate — even though the $150 drug is cheaper for everyone.

What Changed in 2026

Two significant developments are reshaping the prescription drug landscape for Americans this year. First, the first ten Medicare-negotiated drug prices took effect on January 1, 2026 — the result of authority granted to Medicare by the Inflation Reduction Act of 2022. The list includes major medications like the blood thinner Eliquis, the diabetes drug Januvia, and the cancer treatment Imbruvica. Medicare enrollees taking these drugs are paying less than they were in 2025.

Second, the out-of-pocket cap for Medicare Part D enrollees was set at $2,100 for 2026 — meaning no Medicare beneficiary will pay more than $2,100 for covered prescription drugs in a single year, regardless of how expensive their medications are. For seniors managing cancer, multiple sclerosis, or other conditions requiring specialty drugs that can cost $50,000 or more annually, that cap is genuinely life-changing.

The bad news is that while Medicare enrollees are getting some relief, drugmakers raised prices on at least 350 branded medications in January 2026 — with a median increase of around 4%. Pfizer alone raised prices on dozens of drugs. The system that drives prices up has not been fundamentally altered. It has been nudged at the edges.

What You Can Do Right Now

The most powerful tool available to most American patients is one that goes chronically underused: asking for the generic. Generic drugs are FDA-approved to be as safe and effective as their brand-name counterparts and typically cost 80 to 85% less. Asking your doctor or pharmacist whether a generic exists for every prescription you take costs nothing and can save hundreds of dollars annually.

Comparing prices across pharmacies before filling a prescription is equally important. The price of the same drug at the same dose can vary by 300% or more between pharmacies in the same zip code. Tools that aggregate real-time pharmacy pricing have made that comparison faster than it has ever been.

For patients on Medicare, reviewing your Part D plan every year during open enrollment — specifically checking whether your medications’ tier placements have changed — can prevent unexpected cost increases. For patients without insurance, manufacturers’ patient assistance programs, state pharmacy assistance programs, and discount programs available at major retailers can reduce costs significantly for those who qualify.

The system that makes prescription drugs so expensive in America will not be fixed quickly. But navigating it intelligently — knowing the generic options, comparing prices, understanding your coverage — is something every American can do today.