WASHINGTON, APRIL 23, 2026 —

Key Takeaways

- The IRS raised the annual 401(k) contribution limit to $24,500 in 2026, up from $23,500 in 2025 — and workers aged 50 to 59 can now shelter up to $32,500 from taxes by adding the $8,000 catch-up contribution, while workers aged 60 to 63 can reach $35,750 through a special “super catch-up” provision that most Americans don’t know exists.

- A critical rule change took effect in 2026: if you earned more than $150,000 in FICA wages in 2025, your catch-up contributions must now be made as Roth (after-tax) dollars — a shift created by SECURE 2.0 that changes tax planning for millions of higher-income workers who have been pre-tax catch-up contributors for years.

- Only 14% of Americans with a 401(k) actually hit the annual contribution limit — meaning 86% of workers are leaving significant tax-advantaged space unused every year, with compounding consequences that widen over time. A single $24,500 contribution at age 40, assuming historical average returns, grows to more than $265,000 by retirement.

Most Americans know they should contribute more to their 401(k). Most don’t. The gap between knowing and doing is not usually laziness — it is a combination of not understanding the numbers, not knowing the specific rule changes that affect them, and not having a clear picture of what consistent maximization actually does to a retirement date over time. The 2026 limits and rule changes make this the year to close that gap.

The New Numbers for 2026

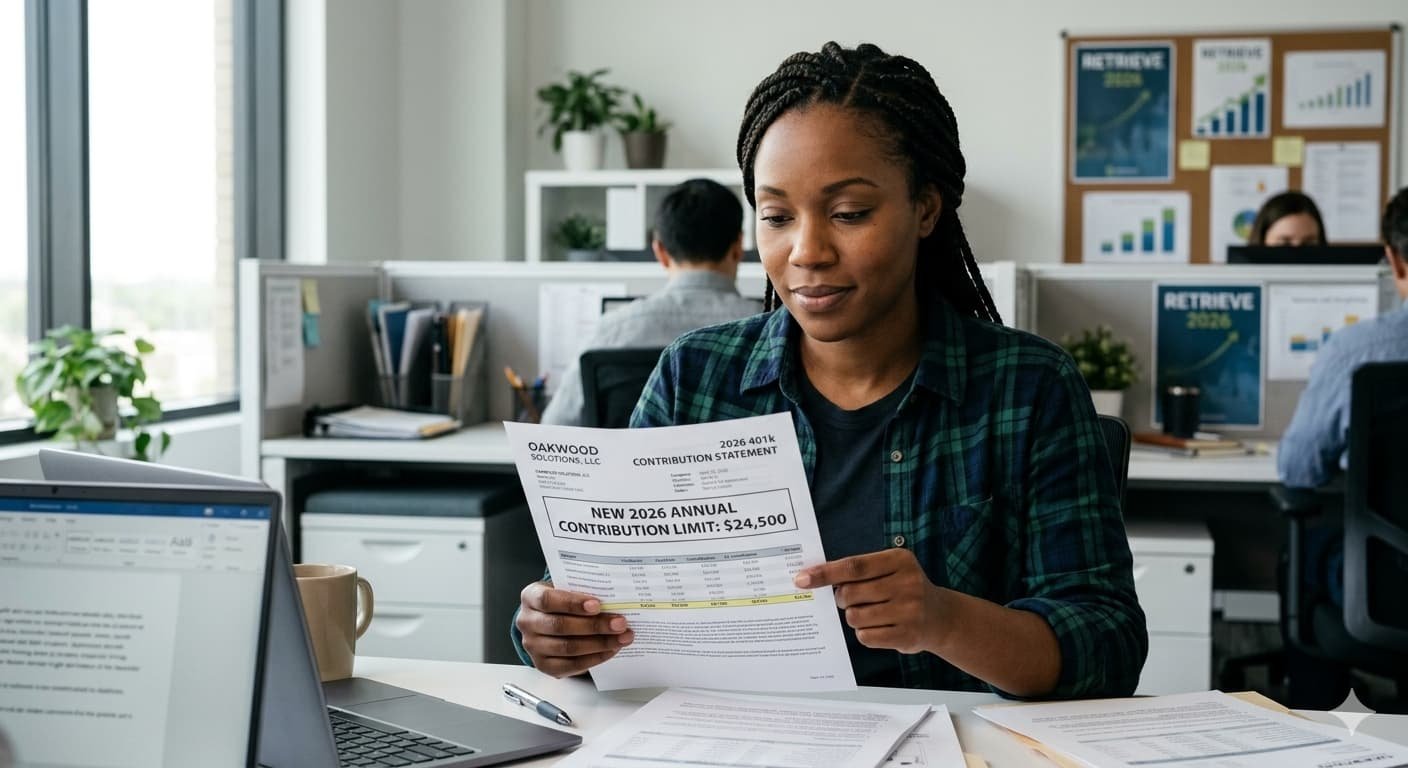

The IRS adjusts retirement plan contribution limits annually for inflation. For 2026, every major limit moved upward — some significantly.

The standard employee contribution limit for 401(k), 403(b), and most governmental 457 plans increased from $23,500 to $24,500. This is the maximum amount you can defer from your paycheck into your employer-sponsored retirement plan this year, regardless of whether those contributions are traditional (pre-tax) or Roth (after-tax). The combined total of traditional and Roth contributions still counts toward this single limit.

The IRA limit — for both traditional and Roth individual retirement accounts — increased from $7,000 to $7,500 for 2026. This limit applies whether or not you also have a workplace plan, though your ability to deduct traditional IRA contributions or contribute to a Roth IRA may be limited by your income.

The overall combined employee and employer contribution limit — the ceiling including your contributions, your employer’s match, profit-sharing contributions, and any after-tax contributions — increased from $70,000 to $72,000 for 2026.

| 2026 Retirement Contribution Limits — Full Picture | 2025 Limit | 2026 Limit |

|---|---|---|

| 401(k) / 403(b) employee contribution | $23,500 | $24,500 |

| Catch-up contribution (ages 50–59 and 64+) | $7,500 | $8,000 |

| Super catch-up (ages 60–63) | $11,250 | $11,250 (unchanged) |

| Total contribution limit (ages 50–59) | $31,000 | $32,500 |

| Total contribution limit (ages 60–63) | $34,750 | $35,750 |

| Combined employee + employer limit | $70,000 | $72,000 |

| IRA / Roth IRA contribution limit | $7,000 | $7,500 |

| SIMPLE plan employee contribution | $16,500 | $17,000 |

The Catch-Up Rules — And the One Most People Miss

Catch-up contributions are the most underutilized tool in retirement planning. Workers aged 50 and over can contribute an additional $8,000 on top of the standard $24,500 limit in 2026, for a total annual contribution of $32,500. Every dollar of that additional $8,000 reduces taxable income by the same amount as a standard contribution — meaning for someone in the 24% federal tax bracket, a full $8,000 catch-up saves approximately $1,920 in federal income taxes in the year it is contributed.

The “super catch-up” provision — one of the lesser-known features of SECURE 2.0 — applies to workers aged 60, 61, 62, and 63 only. These workers can substitute the standard $8,000 catch-up for a higher $11,250 limit, bringing their total annual contribution ceiling to $35,750. The provision exists specifically for workers in the final years before typical retirement ages who feel behind on savings. The window is intentionally narrow — it applies only to those four ages — so workers turning 64 revert to the standard $8,000 catch-up, and workers who have not yet turned 60 cannot access it.

There is an important caveat: not all plans offer the super catch-up. Your plan administrator must elect to allow it. Check with your HR department before planning around this limit.

The 2026 Rule Change That Hits High Earners

This is the change most financial articles are not explaining clearly enough.

Starting in 2026, if your W-2 FICA wages exceeded $150,000 in 2025, any catch-up contributions you make — whether the standard $8,000 or the super $11,250 — must be made as Roth (after-tax) contributions. You cannot make pre-tax catch-up contributions if you fall above this income threshold.

This affects millions of workers who have been making traditional pre-tax catch-up contributions for years and expecting those dollars to reduce their current tax bill. Under the new rule, those workers still get to make the catch-up — but they pay the tax now rather than in retirement. The benefit shifts: instead of a current-year tax deduction, high earners get tax-free growth and tax-free withdrawals in retirement on those catch-up dollars.

There is a critical problem to check immediately: if your plan does not offer a Roth contribution option, high earners above $150,000 may be completely unable to make catch-up contributions in 2026. This is not a theoretical concern — some older workplace plans do not have Roth capability built in. If you earn above the threshold and your plan does not offer Roth contributions, contact your HR or benefits department this week and ask whether the plan has been updated. If it has not, you may need to maximize your IRA contributions separately as an alternative.

What Consistent Maximization Actually Does

The abstract case for maximizing your 401(k) is familiar. The concrete math is more compelling and rarely gets presented with enough specificity to land.

If you are 40 years old and contribute $24,500 in 2026 as a single contribution — assuming a 10% average annual return, consistent with long-term US stock market historical averages — that one year’s contribution grows to more than $265,000 by age 65. Every dollar you contribute this year is worth roughly 10 dollars at retirement for a 40-year-old, 7 dollars for a 45-year-old, and 5 dollars for a 50-year-old. The math decelerates as you age, but it never stops working.

For workers who are behind on savings and approaching the ages that unlock catch-up contributions, the 2026 limits are the most favorable on record for acceleration. A 60-year-old who maximizes the super catch-up for five consecutive years — $35,750 per year from age 60 through 64 — contributes approximately $178,750 in those five years alone, excluding any employer match and excluding the compounding that happens during and after those contributions.

The employer match deserves explicit mention because it is the single most valuable element of most workers’ retirement plans and the most commonly left unclaimed. A standard employer match of 3% to 6% of salary is free money — a 100% immediate return on the matched portion of contributions, before any investment returns are calculated. Failing to contribute at least enough to capture the full employer match is mathematically equivalent to declining a portion of your compensation.

Roth vs. Traditional — The 2026 Framework

The choice between traditional pre-tax and Roth after-tax 401(k) contributions comes down to one question: do you expect your tax rate to be higher now or in retirement? Most financial advisers use this general framework for 2026 given current tax rates and the expected sunset of key provisions of the 2017 Tax Cuts and Jobs Act at the end of 2025 and forward-planning complexity:

Traditional contributions make more sense if you are in a high tax bracket today and expect to be in a lower bracket in retirement — typically workers earning above $150,000 to $200,000 annually who will draw down assets in retirement at lower rates.

Roth contributions make more sense if you are early in your career in a lower tax bracket, if you expect tax rates to rise in future years (a reasonable assumption given long-term federal deficit projections), or if you want tax-free income in retirement to manage future tax bracket flexibility.

Both types can coexist in the same plan and count toward the same annual limit, so many workers split their contributions between them.

Pro Tips a Generic Article Would Miss

1. The 1% annual increase strategy beats annual discipline by a wide margin. Most people fail at saving more by trying to dramatically increase their contribution rate all at once. The research-backed approach is to increase your contribution rate by exactly 1% each year — and specifically to time that increase to coincide with your annual raise. Because the raise and the increase happen simultaneously, your take-home pay does not feel like it has dropped. Over a decade, this auto-escalation strategy alone can increase your retirement balance by 30% to 50% versus maintaining a flat contribution rate.

2. Check whether your plan accepts after-tax contributions beyond the $24,500 limit. Many workers do not know that some 401(k) plans allow what is called a “mega backdoor Roth” — after-tax contributions above the standard deferral limit that can then be converted to Roth status. The ceiling for total contributions (employee plus employer plus after-tax) is $72,000 in 2026. If your plan allows after-tax contributions and in-service Roth conversions, a worker under 50 whose employer contributes $20,000 in matching could add up to $27,500 in additional after-tax contributions — creating a massive Roth account with tax-free growth potential. Ask your HR department specifically whether your plan allows both after-tax contributions and in-plan Roth conversions.

3. Old 401(k)s from previous jobs are the most commonly forgotten retirement assets in America. Before adjusting your current contribution strategy, run a search of your employment history and confirm that every 401(k) from every previous employer has been located and accounted for. Forgotten plans stay invested — sometimes well, sometimes poorly, often in default funds — and consolidating them into your current plan or a rollover IRA gives you clarity and control over your full retirement picture.

Maximizing your 401(k) in 2026 is not about being wealthy. It is about using the specific rules available to you this year — the new $24,500 limit, the catch-up provisions, the Roth rule change if it applies, and the compounding math that rewards every dollar contributed today with many more dollars at retirement. The window for 2026 contributions closes December 31. The decisions made before then have a longer tail than most workers realize.