WASHINGTON, MARCH 20, 2026 —

Key Takeaways

- 72 million Americans — 41% of working-age adults — currently have medical bill problems or unpaid medical debt according to The Commonwealth Fund

- $194 billion in medical debt is currently in active collection across the United States — making healthcare the single largest source of consumer debt after mortgages

- Most Americans don’t know they have the legal right to negotiate, dispute, and reduce their medical bills — often by 40% to 60% or more

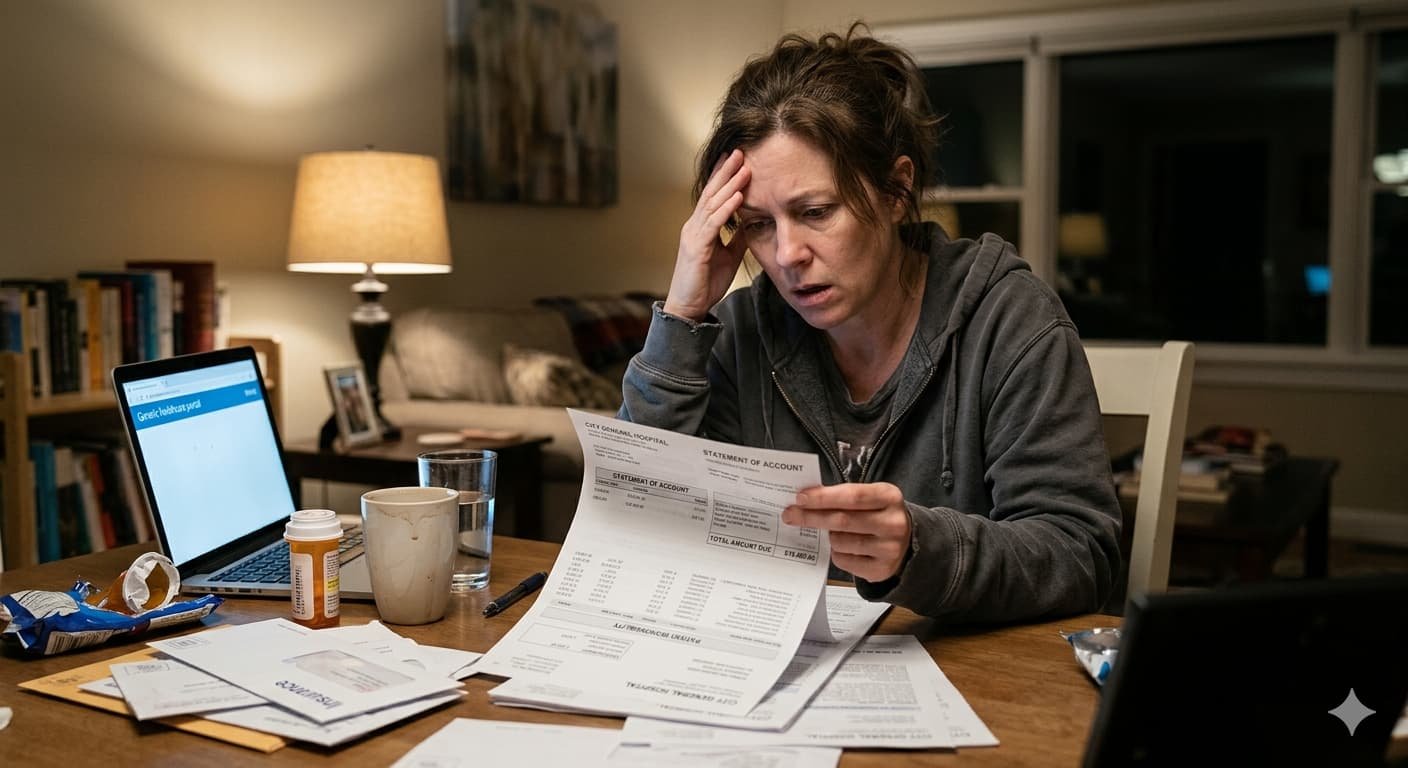

You did everything right. You have health insurance. You went to an in-network hospital. You followed the rules. And then a bill arrived in your mailbox for $11,000 — and nobody can explain exactly why.

This is the medical debt experience for tens of millions of Americans. Not reckless spending. Not willful avoidance. Just the collision between a medical emergency and a billing system so complex that even hospital administrators struggle to explain it. 72 million Americans are currently dealing with medical bills they cannot fully pay. The system that created those bills is not going to fix itself. But there are concrete, proven steps you can take right now to reduce, dispute, or eliminate what you owe.

The Scope of the Problem in 2026

Medical debt in America is not a niche issue. It is the defining financial crisis of the American middle class — and it is getting worse.

| Medical Debt Level | % of Americans Affected | Common Cause |

|---|---|---|

| Under $500 | 45% of debt holders | Urgent care, copays, outpatient visits |

| $1,000 — $5,000 | 32% of debt holders | Surgery, ER visits, diagnostic testing |

| $5,000 — $10,000 | 20% of debt holders | Hospitalizations, chronic conditions |

| Over $10,000 | 3% of debt holders | Major surgery, cancer treatment, long-term care |

The numbers behind those percentages are staggering. A peer-reviewed study published in the journal JAMA found that $194 billion in medical debt was in active collection across the United States. That figure does not include bills still being paid directly to providers, medical expenses put on credit cards, or loans taken out to cover healthcare costs. The real total is significantly higher.

Half of all Americans who report difficulty paying their bills cite medical costs as the primary reason. Medical debt is the leading cause of personal bankruptcy in the United States — a fact that has not changed in more than two decades despite the passage of the Affordable Care Act, the expansion of Medicaid, and the creation of hospital financial assistance programs that most patients never find out about.

Why Hospital Bills Are Almost Never Final

The single most important thing most Americans don’t know about medical billing is this: the number on your bill is not the number you have to pay.

Hospitals set their list prices — called chargemaster rates — at levels that bear almost no relationship to what insurers actually pay or what uninsured patients can reasonably afford. A procedure billed at $15,000 might be settled by an insurer for $3,200. An uninsured patient who simply pays the bill without question pays $15,000. The same patient who calls the billing department and asks for the self-pay rate — the discounted rate hospitals are required by law to offer uninsured patients — might pay $4,500.

The difference between those two outcomes is one phone call.

Errors Are More Common Than Most Patients Realize

Medical billing errors are not rare exceptions. They are routine. Studies have found that up to 80% of medical bills contain at least one error — duplicate charges, incorrect diagnosis codes, charges for services never rendered, and items billed under the wrong insurance. Every one of those errors can be disputed.

You have the legal right to request an itemized bill — a line-by-line breakdown of every charge — from any healthcare provider. Most hospitals do not offer this automatically. You have to ask. When you receive it, compare every line item against your explanation of benefits from your insurer. Discrepancies between what the hospital says it charged and what your insurer says it paid are grounds for a formal dispute.

Common Misconceptions

Misconception 1: “If my bill went to collections my credit is already ruined.” Not necessarily. As of 2023, medical debt under $500 was removed from all credit reports by the major bureaus. Medical debt under $500 no longer affects your credit score at all. The Consumer Financial Protection Bureau has proposed removing all medical debt from credit reports — a rule that remains under consideration in 2026.

Misconception 2: “I make too much money to qualify for financial assistance.” Almost certainly wrong. Most nonprofit hospitals — which make up the majority of U.S. hospitals — are legally required to maintain charity care programs. Income thresholds for these programs often extend well into the middle class. A family of four earning up to $93,000 qualifies for financial assistance at many major hospital systems.

Misconception 3: “Once I pay the bill I can’t dispute it.” Wrong. You can dispute a medical bill after payment and request a refund if errors are found. Statutes of limitations on disputes vary by state but are typically two to four years.

Pro Tips a Generic Article Would Miss

Pro Tip 1: Before you pay any bill over $500, call the hospital billing department and ask three specific questions: Is there a self-pay discount available? Do you have a financial assistance program? Can I set up a zero-interest payment plan? All three options exist at most U.S. hospitals — none of them will be offered to you unless you ask.

Pro Tip 2: Medical billing advocates — professionals who review and negotiate medical bills on your behalf — typically work on contingency, taking 25-35% of whatever they save you. On a $20,000 bill they reduce to $8,000, you pay them $3,000 and keep $9,000. For large bills, this is almost always worth exploring.

Pro Tip 3: If your debt has been sold to a collection agency, you have significantly more negotiating power than you realize. Collection agencies typically purchase medical debt for 4 to 7 cents on the dollar. An agency that bought your $10,000 debt for $600 has enormous room to settle — and many will accept 20 to 30 cents on the dollar rather than pursue lengthy collection efforts.

Actionable Step

Pull out every outstanding medical bill you have right now. For any bill over $200, call the provider’s billing department this week and request three things: an itemized bill, information about financial assistance programs, and the self-pay or prompt-pay discount rate. You do not need a lawyer. You do not need a special program. You need to ask — clearly, politely, and persistently. Most Americans who do this reduce their bills. Most Americans who don’t, pay the full amount. The difference is entirely in whether you make the call.

Medical debt in America will not be solved by a single policy change or a single phone call. But for the 72 million Americans carrying it right now, the path forward starts with understanding that almost every bill is negotiable — and that the first person who needs to know that is you.