WASHINGTON, May 20, 2026 —

More Americans filed for bankruptcy in the first three months of 2026 than in any first quarter since the pandemic disrupted the courts in 2020. The numbers are not the result of a single catastrophic event. They are the accumulated weight of three years of inflation, five years of rising consumer debt, and an interest rate environment that turned every variable-rate obligation in America into a compounding problem.

According to American Bankruptcy Institute data compiled from the U.S. Courts system, 150,009 bankruptcy petitions were filed in the first quarter of 2026 — up 14% from 132,094 in the same period a year earlier. The acceleration spans every major filing category: consumer, commercial, and small business. Household debt has reached $18.8 trillion. Delinquency rates across all outstanding balances have worsened to 4.8%. Credit card delinquencies, mortgage late payments, and student loan defaults are all rising simultaneously.

For the millions of Americans watching this data point from inside their own financial situation, the practical question is not whether filings are rising. It is what bankruptcy actually does, which version applies, and what it costs to find out.

What Chapter 7 Does — and the Four-Month Clock That Changes Everything

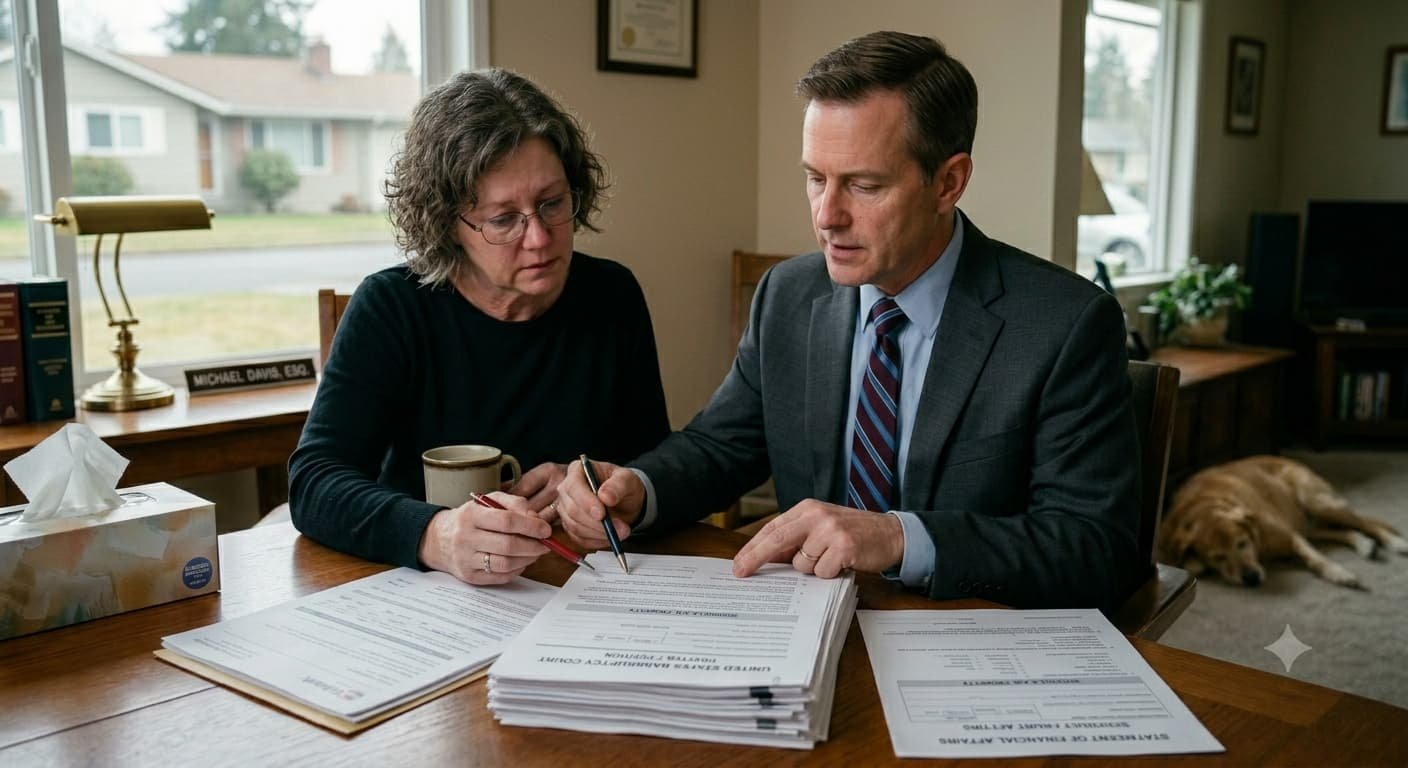

Chapter 7 is the form of bankruptcy that most Americans picture when they hear the word. Its technical name is liquidation bankruptcy, but in practice, more than 95% of Chapter 7 cases are what attorneys call no-asset filings — meaning the debtor keeps essentially all of their possessions through federal or state exemptions and walks away with their qualifying unsecured debts eliminated entirely.

The debts Chapter 7 can discharge include credit card balances, medical bills, personal loans, utility arrears, most civil lawsuit judgments, and unpaid rent from a prior lease. The debts it cannot discharge include federal and most state taxes, alimony and child support obligations, student loans in most circumstances, and debts arising from fraud or willful harm.

The timeline is its most important feature. Chapter 7 cases typically complete in three to five months from filing to discharge. The moment a petition is filed, an automatic stay takes effect — stopping all collection calls, wage garnishments, lawsuits, and foreclosure proceedings immediately. For a person facing a garnishment of their paycheck or a creditor lawsuit scheduled for the following week, that automatic stay is the single most valuable legal protection available without requiring a court hearing.

The entry cost for Chapter 7 in 2026 is a $338 filing fee plus attorney fees that typically run between $1,500 and $3,500 depending on the complexity of the case. The attorney fee is almost always paid upfront — because once a bankruptcy is filed, attorneys generally cannot collect from a discharged client.

The primary gate is the Means Test. To qualify for Chapter 7, a filer’s gross household income must fall below their state’s median income for a household of their size, or pass a second formula based on IRS-standard expenses that can still qualify higher-income filers depending on their specific debt load and secured obligations. The income figures are updated twice annually. In 2026, rising state median income figures have actually made it easier for some households to qualify for Chapter 7 than in prior years — a counterintuitive benefit of wage growth in an inflationary environment.

What Chapter 13 Does — and Why Homeowners in Trouble Need to Know It Exists

Chapter 13 is the version of bankruptcy that most people do not know they need until it is the only option that saves their home. It does not wipe out debt in four months. It restructures it across a three-to-five-year repayment plan that the court approves based on the filer’s disposable income after essential living expenses.

The central feature of Chapter 13 that no other tool replicates: it allows a debtor to catch up on mortgage arrears through the bankruptcy plan while keeping the house. A homeowner who is $24,000 behind on their mortgage — an amount that would normally trigger imminent foreclosure — can propose a Chapter 13 plan that spreads those arrears over 60 months at $400 per month, while continuing to make their current mortgage payment. The foreclosure stops the moment the petition is filed. The arrears get resolved inside the plan. At the end of five years, if the plan is completed, remaining eligible unsecured debts are discharged.

Chapter 13 also applies to filers whose income is too high to qualify for Chapter 7 under the Means Test. In 2026, the debt eligibility ceilings for Chapter 13 allow filers with unsecured debts below $526,700 and secured debts below $1,580,125 to file — thresholds that cover the vast majority of American households facing serious financial distress.

The cost is higher. Chapter 13 filing fees run $313 and attorney fees typically range from $3,000 to $5,500, spread across the plan in most cases. The commitment is three to five years of court-supervised monthly payments. The completion rate for Chapter 13 plans runs between 33% and 40% nationally — meaning most filers who start the process do not finish it. Understanding why that completion rate is low before filing is as important as understanding what the plan offers.

| Chapter 7 vs. Chapter 13 — 2026 Quick Reference | Chapter 7 | Chapter 13 |

|---|---|---|

| Type | Liquidation | Reorganization |

| Timeline | 3–5 months | 3–5 years |

| Unsecured debt outcome | Discharged | Partially repaid, remainder discharged |

| Home foreclosure protection | Stops temporarily; doesn’t cure arrears | Cures arrears over plan period |

| Income requirement | Must pass Means Test | Must have regular income |

| Can catch up on mortgage arrears | No | Yes |

| Filing fee (2026) | $338 | $313 |

| Typical attorney fee | $1,500–$3,500 | $3,000–$5,500 |

| Credit report impact | 10 years | 7 years |

| Student loans discharged | Rarely | Rarely |

| Taxes discharged | Usually not | Usually not |

| Q1 2026 filings | 89,259 (up 17% YoY) | 51,962 (up 8% YoY) |

The Fastest-Growing Demographic Filing — and Why It Matters

The Consumer Bankruptcy Project’s research produces a figure that rarely makes headlines but defines the human reality of the current surge: the fastest-growing group of bankruptcy filers in America is adults 65 and older. They now represent 18.7% of all filers — up from 4.5% in 2001. The median age of all filers is 49.

The explanation is structural. Older Americans are more likely to carry medical debt — the single most common trigger for personal bankruptcy filings — and less likely to have the income trajectory to service that debt after retirement. Social Security benefits, while inflation-adjusted, have not kept pace with healthcare cost inflation. The Medicare Part B premium increases, the erosion of supplemental benefits from Medicare Advantage plans, and the absence of any cap on out-of-pocket costs for extended illnesses have all contributed to a financial environment where a serious health event in retirement can rapidly become a bankruptcy-level debt load.

The second structural driver is the lag that bankruptcy professionals consistently identify between economic conditions and filing behavior. Americans resist filing for bankruptcy as long as possible — depleting savings, borrowing from family, taking on additional credit, and selling assets before acknowledging that the math has stopped working. The Q1 2026 surge reflects economic pressures that began building in 2023 and 2024, not conditions that arose overnight.

Pro Tips a Generic Article Would Miss

1. The credit score recovery after Chapter 7 is faster than most people believe — and the window to buy a home afterward is shorter than most attorneys mention. A Chapter 7 bankruptcy stays on a credit report for 10 years. But credit score recovery begins almost immediately after discharge, because the discharged debt-to-income ratio improves dramatically in a single event. Most filers see meaningful score improvement within 12 to 24 months by using secured credit tools and maintaining perfect payment history on any remaining obligations. For homebuyers specifically: FHA loans become available just two years after a Chapter 7 discharge. Conventional mortgage financing through Fannie Mae and Freddie Mac becomes available four years after discharge. The retirement income planning implication is real — filing at 52 rather than 57 can mean the difference between being mortgage-eligible at 54 and waiting until 61.

2. The automatic stay is the most powerful short-term tool in consumer finance — and most people don’t know they can access it in a single day. The moment a bankruptcy petition is filed, every collection action against the debtor stops by operation of federal law. Wage garnishments halt. Collection calls stop. Scheduled foreclosure sales are paused. Pending civil lawsuits are frozen. This happens automatically — not after a hearing, not after a judge reviews the case, but the instant the petition is filed and timestamped by the court. For a debtor facing an imminent paycheck garnishment or a foreclosure sale scheduled for the following morning, emergency Chapter 7 or Chapter 13 petitions can be filed with only a list of creditors — the full supporting schedules can be filed within 14 days. Most bankruptcy attorneys will handle emergency filings with same-day or next-day turnaround.

3. The Means Test income calculation uses a six-month look-back — and the timing of your filing can determine whether you qualify for Chapter 7 or are forced into Chapter 13. The Means Test calculates your average monthly income over the six calendar months before you file. If you recently lost a job, took a significant pay cut, or had a major income reduction, your current income may be much lower than the six-month average the Means Test will use. In some cases, waiting 30 to 60 additional days after an income event — until the lower income is reflected across more of the six-month window — shifts the Means Test result from Chapter 13 required to Chapter 7 eligible. This timing consideration is one of the most valuable things a bankruptcy attorney can evaluate before filing, and it is almost never mentioned in generic guides to the bankruptcy process.

FAQ

Q: Will bankruptcy stop wage garnishment immediately? A: Yes. The automatic stay takes effect the moment a bankruptcy petition is filed and stops all wage garnishments immediately by federal law. If you are currently having wages garnished, filing a bankruptcy petition — even an emergency one with only a creditor list — stops the garnishment the same day. Your employer must be notified of the filing and must release the garnishment hold upon receiving that notice.

Q: Can I keep my house if I file for bankruptcy? A: It depends on which chapter you file and the status of your mortgage. In Chapter 7, the automatic stay temporarily pauses foreclosure, but Chapter 7 does not cure mortgage arrears. If you are current on your mortgage, you can typically keep your home by continuing to make payments. If you are behind on your mortgage and want to save your home, Chapter 13 is the tool that allows you to catch up on arrears over a three-to-five-year plan while keeping the property.

Q: How long does bankruptcy stay on your credit report? A: Chapter 7 bankruptcy stays on a credit report for 10 years from the filing date. Chapter 13 stays for 7 years. Both negatively affect your credit score, but the impact diminishes over time, particularly as positive payment history is built after filing. Most filers see meaningful score improvements within 12 to 24 months of discharge if they use secured credit tools and maintain consistent on-time payments.

Q: What debts cannot be discharged in bankruptcy? A: Several categories of debt survive bankruptcy regardless of which chapter you file. Federal and most state income taxes from the last three years, alimony and child support, student loans in most circumstances, debts arising from fraud or intentional harm, and fines owed to government agencies are not dischargeable. Child support and alimony also receive priority treatment in Chapter 13 plans and must be paid in full before the plan is approved.

Q: Do I need an attorney to file for bankruptcy? A: You are legally permitted to file for bankruptcy without an attorney — called filing pro se — but the process is procedurally complex and errors can result in case dismissal or loss of the automatic stay. The American Bankruptcy Institute and National Consumer Law Center both recommend attorney representation, particularly for Chapter 13 cases, which require a feasible multi-year plan that must survive creditor objections and trustee review. Many bankruptcy attorneys offer free initial consultations, and Chapter 7 attorney fees are typically lower than a single month of the debt payments the discharge will eliminate.

If your monthly debt payments are exceeding your ability to cover basic living expenses, the first step is not filing a bankruptcy petition — it is a free initial consultation with a bankruptcy attorney or a nonprofit credit counseling agency. Federal law requires that anyone considering bankruptcy speak with an approved credit counseling agency within 180 days before filing. That conversation is free, takes approximately an hour by phone, and will tell you whether bankruptcy is necessary or whether a debt management plan, negotiated settlement, or income-based repayment arrangement could resolve the problem without a court filing. The answer may surprise you. One in ten Americans eventually files. Most of them waited longer than they should have.